If you’re an overseas company selling goods, providing digital services, or using marketplaces, VAT compliance is critical to avoid blocked imports, penalties, and service interruptions. In this Belgium VAT registration guide, let’s find the answers to the most frequently asked questions, including registration triggers, thresholds, input-tax refunds, and deregistration rules.

Why Non-Resident Firms Must Register for VAT in Belgium?

Failing to complete the VAT registration in Belgium can lead to severe penalties, blocked marketplace access, and customs clearance delays that disrupt your supply chain. For foreign companies selling goods or services in Belgium, compliance is mandatory.

When Does a Foreign Business Need to Register? Key Triggers

VAT registration for non-resident businesses in Belgium is crucial under the following circumstances:

- Holding stock in Belgium: If you store goods in a Belgian warehouse for local distribution.

- Supplying digital services to Belgian consumers: All B2C digital service providers must register regardless of threshold.

- Importing goods into Belgium for local sale: Import VAT applies, and registration is needed for compliance.

- Marketplace facilitation rules: Platforms often require sellers to have a valid Belgian VAT number to continue selling.

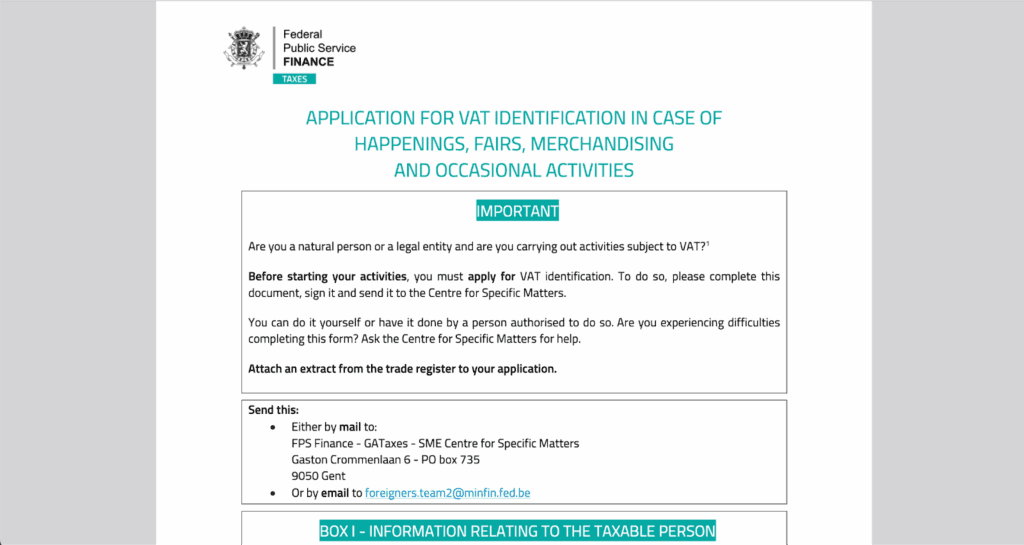

- Participating in trade shows or events: If you sell goods on-site during an event or exhibition.

Registration Thresholds & Nexus Tests

Understanding when to go for VAT registration for foreign companies in Belgium is crucial. Here’s what you need to know:

- No Threshold for Non-Residents (“Nil Threshold”): Foreign businesses must register for VAT immediately upon making any taxable supply in Belgium, regardless of turnover. There is no minimum threshold applicable to non-resident entities.

- Digital Services & EU OSS Option: EU-based digital service providers (B2C) benefit from a €10,000 EU-wide turnover threshold, above which they can either register in Belgium or opt into the EU One-Stop Shop (OSS) regime to simplify reporting.

- Imports, Local & Reverse-Charge Supplies: Any imports into Belgium for resale or domestic supply trigger immediate VAT compliance and require VAT registration.

- Fiscal Representative & Bank Guarantee (Non-EU Only): Non-EU businesses must appoint a Belgian fiscal representative, and provide a bank guarantee/cash deposit to secure their VAT liabilities, typically 10% of estimated annual VAT, with a minimum of €7,500 and a maximum of €1 million.

Belgium VAT Number Format Explained

Belgium assigns a unique BTW-nummer / Numéro de TVA for businesses registered for VAT. Here’s what you need to know:

- Format: BE + 10 digits

- Example: BE 0123 456 749

- The first digit is always 0, followed by 9 other digits.

- Total length (with country prefix): 12 characters (including BE).

Belgium uses the ISO 7064 MOD 97-10 checksum. The last two digits of the VAT number are a check number, calculated from the preceding eight digits.

Formula: Check = 97 – (First 8 digits mod 97)

Example: If the base number is 012345674, then

97 – (1234567 mod 97) = 49

So full VAT number = BE 0123 456 749.

Is a Local Tax Agent or Fiscal Representative Required?

In Belgium, non-EU businesses are required to appoint a fiscal representative to handle VAT compliance. This representative must be approved by the Belgian VAT authorities and is jointly and severally liable for the VAT obligations of the non-resident business.

Who needs it?

- Non-EU companies: Mandatory fiscal representative.

- EU companies: No representative required, but a local VAT agent is optional.

The fiscal representative is fully liable for VAT debts and penalties, which makes the selection of a reliable partner critical. A financial guarantee (often around €7,500 or more, depending on expected VAT liability) is typically required by the Belgian tax authorities before approving the representative.

Special Schemes & Simplifications

Belgium offers several special VAT regimes that can simplify compliance for foreign businesses:

- Import VAT Deferment: Businesses can apply for a license that allows them to defer payment of import VAT and report it in their periodic VAT return instead of paying at customs. This improves cash flow significantly.

- OSS for E-Services: Non-EU businesses supplying digital services to Belgian consumers can use the Non-Union OSS scheme to declare VAT in a single EU return, avoiding multiple registrations.

- Customs Warehousing & Consignment Stock: Belgium has customs-approved warehousing schemes allowing goods to be stored without incurring import VAT until they are released for sale. This is beneficial for e-commerce sellers using Belgian fulfillment centers.

Step-by-Step: How to Register for VAT in Belgium

Here is the step-by-step guide to register for VAT online in Belgium:

1. Check if You Meet the Registration Obligation: Verify if your business triggers Belgian VAT registration.

2. Gather Required Documents: Prepare your company certificate, proof of foreign registration, identification of directors, and Belgian fiscal rep details.

3. Create an Account on the Intervat Portal or Complete Form 604A: Log in to Intervat or submit Form 604A for non-residents.

4. Upload Documents & Submit Application: Attach all required documents, including identification and proof of activity, and submit for processing.

5. Pay Any Applicable Government Fees: Belgium usually does not charge a registration fee, but check for changes in regulations.

6. Receive Your Belgian VAT Number: Once approved, you will receive an 11-digit VAT number (starting with “BE”).

Required Documents Checklist

Prepare the following documents:

- Certificate of Incorporation

- Directors’ Identification

- Proof of Business Activity

- Bank Letter

- Signed Power of Attorney

Processing Time & Government Fees

Processing typically takes 2 to 4 weeks from submission of complete documents. Delays may occur if additional clarifications or translations are required by the Belgian VAT authorities. There is no direct registration fee for obtaining a Belgian VAT number.

Post-Registration Obligations in Belgium

Foreign businesses registered for Belgian VAT must comply with the following ongoing obligations:

- VAT Return Filing Frequency:

- Monthly: Default for most non-resident businesses.

- Quarterly: Allowed only if annual turnover is below €2,500,000 and conditions are met.

- Payment Deadlines: VAT returns and payments are generally due by the 20th day of the month following the reporting period.

- Currency Conversion: Non-EUR transactions must be converted using the European Central Bank (ECB) exchange rate applicable on the invoice date or reporting period end.

- Record-Keeping: VAT-related records must be retained for at least 7 years (extended to 15 years for real estate transactions).

- Intrastat & EC Sales Listings: Required for intra-EU trade above thresholds.

Claiming Input-Tax Credits & Refunds as a Non-Resident

Non-resident tax registration Belgium can generally recover input VAT on local purchases, provided the expenses are linked to taxable supplies in Belgium. Here’s what you need to know:

Eligibility

- Must be a VAT-registered non-resident business in Belgium.

- Expenses must relate to Belgian taxable transactions (e.g., local sales, warehousing, imports).

- Input VAT on entertainment, passenger cars, and non-business expenses is non-recoverable.

Documentation Standards

- Original or electronic VAT invoices issued in compliance with Belgian invoicing rules.

- Proof of import VAT payment (customs documentation if applicable).

- Proper accounting records matching invoices and declarations.

Refund Timelines

- Input VAT is normally offset in the next VAT return.

- For businesses using the EU Refund Directive (for EU claimants) or 13th Directive procedure (non-EU claimants), the refund process can take 4–8 months after submission.

Penalties for Late Registration or Non-Compliance

Failing to meet VAT obligations in Belgium can result in serious financial and operational consequences. Here’s what foreign businesses, especially non-residents, need to know:

- Late Registration: €500 flat fine for failing to register. Additional €100 per month, capped at €500.

- Late or Non-Submission of VAT Returns: €100 per month delay, up to €500 total. €500 for first missed return, rising to €5,000 per violation for repeated offenses.

- Incorrect or Incomplete Returns: €80 for minor irregularities. €500 for serious omissions.

- Late or Non-Payment of VAT: 5% penalty if VAT is reported on time. 10% if the VAT return is filed late. 15% if the tax arises from a “substitute” VAT return.

- Interest on Late Payments: Typically charged at 0.66% per month (~8% annually).

Deregistration & VAT Number Changes in Belgium

When your foreign business ceases VATable operations in Belgium or needs to update your VAT details, it’s vital to follow the correct procedure to stay compliant and avoid penalties.

Deregistration is required if:

- You no longer conduct VAT-taxable activity in Belgium (e.g., cease supplies, close inventory, end e-service sales).

- You’re restructuring your business, merging, or discontinuing Belgian operations.

Updates needed when:

- Changing your business address, legal name, or representative.

- Transitioning from a branch to a standalone entity or vice versa.

Conclusion

VAT compliance in Belgium is a critical requirement for foreign businesses engaged in cross-border trade, digital services, or local supply chains. Failing to register on time can lead to penalties, blocked imports, and disruptions in marketplace operations. By understanding thresholds, registration steps, and ongoing obligations, your business can avoid unnecessary risks and maintain smooth operations in the EU market.

Need expert assistance? Commenda can help with VAT registration, fiscal representation, and compliance in Belgium, ensuring a hassle-free process from start to finish. Book a demo today.